A route-map on how European and global sustainability standards for corporate reporting can and will converge

By Richard Howitt, Senior Advisor at Frank Bold and former CEO of the International Integrated Reporting Council, Reuters

April 13, 2022

The fragmented patchwork of different ways for companies to report and be held to account on their social and environmental performance is soon to be replaced by widely accepted and endorsed international standards for corporate sustainability.

The European Union announced its decision to develop such standards in January 2020, followed by the International Financial Reporting Standards (IFRS) Foundation proposing the development of global standards in October, later in the same year.

The question on the lips of policymakers, companies, investors and stakeholder groups is how will these two initiatives inter-relate? Will this represent a new fragmentation or can they be complementary? Will and should they converge into one?

What are the key differences of approach?

As the respective bodies developing the new standards - the European Financial Reporting Advisory Group (EFRAG) and the fledgling International Sustainability Standards Board (ISSB) - establish arrangements for coordination between themselves, the basic differences between the two approaches are clear.

European standards build on EU policy and legislative programmes including the Green Deal, its taxonomy and investor disclosure requirements for sustainable finance, and will be immediately linked to regulatory requirements, via the EU’s Corporate Sustainability Reporting Directive that will become applicable to over 50 000 largest EU companies.

The global standards are aimed at all jurisdictions worldwide, intended to be applicable in different cultural, business, legal and regulatory environments and may remain voluntary over an extended period, as the pace of implementation will depend on the discretion of regulators in different countries over time.

The ISSB has made an explicit commitment to starting with climate disclosures, whereas EFRAG is seeking a more comprehensive approach, putting emphasis on the interdependence between different environmental, social and governance (ESG) impacts from companies, whilst also providing a robust climate standard itself.

The global standards are based on an ‘enterprise value creation’ or financial materiality approach, in which sustainability impacts are measured in terms of impacts on the financial position and prospects of the company itself.

European standards are being developed based on the ‘double materiality’ principle, where disclosure is required both from the point of view of financial impact on the company and on the impact of the company on society and the environment.

This has been described as the difference between ‘outside in’ and ‘inside out’.

As with financial reporting, investors are intended to be the primary users of reports produced under ISSB standards, whereas the European standards seek reports aimed at both investors and a wider range of stakeholder groups.

However, these differences should not obscure the fact that both initiatives are a response to the same extensive and persistent demands from business, capital markets and stakeholders for unified standards to enable company sustainability performance to be reported, comparable and rewarded.

Perhaps it is also the proximity of the developments in response both in Europe and at the global level - astonishingly fast in comparison to the highly measured pace in the world of financial reporting standards - which exposes the catalytic effect that each is having on the other.

In the face of the imperative for the world to move far more rapidly to combat climate change and social instability, the existence of both initiatives might actually be creating a combined effect, which together will help companies transform to the sustainable business models that are essential to humanity.

Lines of communication

At a structural level, the ISSB and EFRAG have quickly begun to establish necessary lines of communication.

The ISSB plans to involve the EU in its multi-stakeholder consultative committee, designed to involve representatives from different jurisdictions around the world.

The European Union has already held two formal meetings with international sustainability standard-setting initiatives.

For those worried about duplication, these are positive signs. However, there remains a lack of synchronisation in how the two approaches may develop.

The conception for the ISSB is that it will form a common baseline of standards to ensure consistency and comparability around the world. Different regions could add standards according to this approach - including Europe - where they have different policy goals. The ISSB is seen to be very much driving the development of the new sustainability standards.

EU standards should indeed aim to incorporate the essential elements of globally accepted standards, according to the European Commission. However, the European approach envisages a process of ‘co-construction’ between the initiatives, with Europe contributing as much as adding to the ISSB’s work, in a spirit of two-way cooperation and mutual dialogue.

This may all neatly be summed up between the ISSB being firmly in the driving seat, but the European Union not being willing to simply be a passenger.

The European approach has also committed to assessing the international standards on a continuing basis and to be ready to adapt European standards accordingly. However, this commitment is envisaged to take place only at the end of successive three yearly periods. The proposals for the ISSB are for discussion between jurisdictions, but with no timetable for action in response.

This suggests the two bodies may remain committed to developing standards within their own distinct governance, and that alignment between the two will only proceed on an ‘ex post’ basis, at perhaps too slow a pace to meet industry demands.

A different analogy borrowed from the laws of physics, is that objects can repel or attract each other. Let us start with what may be seeking to push the European and global initiatives apart.

What are the forces behind divergence?

First and foremost, governance arrangements which have and are being painstakingly created in each respective initiative, are a key source of difference which will be difficult to overcome.

Quite simply, the standard-setters are answerable to very different bodies, which are bound to develop their own built-in momentum, irrespective of any (albeit genuine) expressions of goodwill between them.

The accountancy company EY has said that it believes divergence to be inevitable, pointing to the stricter environmental and social standards which exist in Europe compared to the rest of the world. This perspective suggests that the European approach is needed to secure higher standards, whereas the need to secure acceptance across the world puts the global standards at risk of being drawn to the lowest common denominator.

Many also point to Europe’s proposed Carbon Border Adjustment Mechanism, in which importers will have to comply with Europe’s higher environmental standards - including in corporate reporting - or face extra tariffs to ensure no competitive disadvantage to European business.

In essence, this means European sustainability standards would not simply apply to EU-based subsidiaries of foreign-owned firms, but also to overseas companies who simply want to trade in Europe’s Single Market. For a large part of the world’s economy, these factors may mean that European standards become de facto global standards, based on Europe’s trade power.

Meanwhile, the different definitions of determining the materiality in what should be reported by companies between the European and global standards, have been seen by some as the biggest obstacle between the two.

Companies may be tempted to believe they can ‘cherry pick’ selective standards picked from both initiatives, would fail to understand that this would fall short of the structured reporting which is required by investors and the comparability favoured by all. For companies covered by the EU standards, these will be mandatory in any case.

Interestingly, many investors including the industry-leading UN-supported Principles for Responsible Investment representing nearly 5,000 investors worldwide, advocate for sustainability reporting which addresses both the sustainability performance of the company and the financial materiality of its sustainability impacts together, appearing to favour the European approach.

The umbrella organisation of ESG investors in Europe, has argued that the disclosure of the right information must be the aim, not to be achieved at the expense of the quest for global harmonisation.

A forceful logic behind the position of investors is that they believe data on impacts is necessary to enable assessment of financial materiality in the first place. Therefore it is integral to the aim of enterprise value creation in any case.

Despite these differences, in developments which have been driven by the need for sustainability information from companies to be far more coherent, consistent and comparable, it is important not to underestimate the strong forces which may cause the global and the European standards to actually converge.

The forces for convergence

The accelerated pace towards standard-setting for corporate sustainability reporting is a result in both the urgency of sustainability challenges and in particular in a huge change in investor opinion in favour of making it happen.

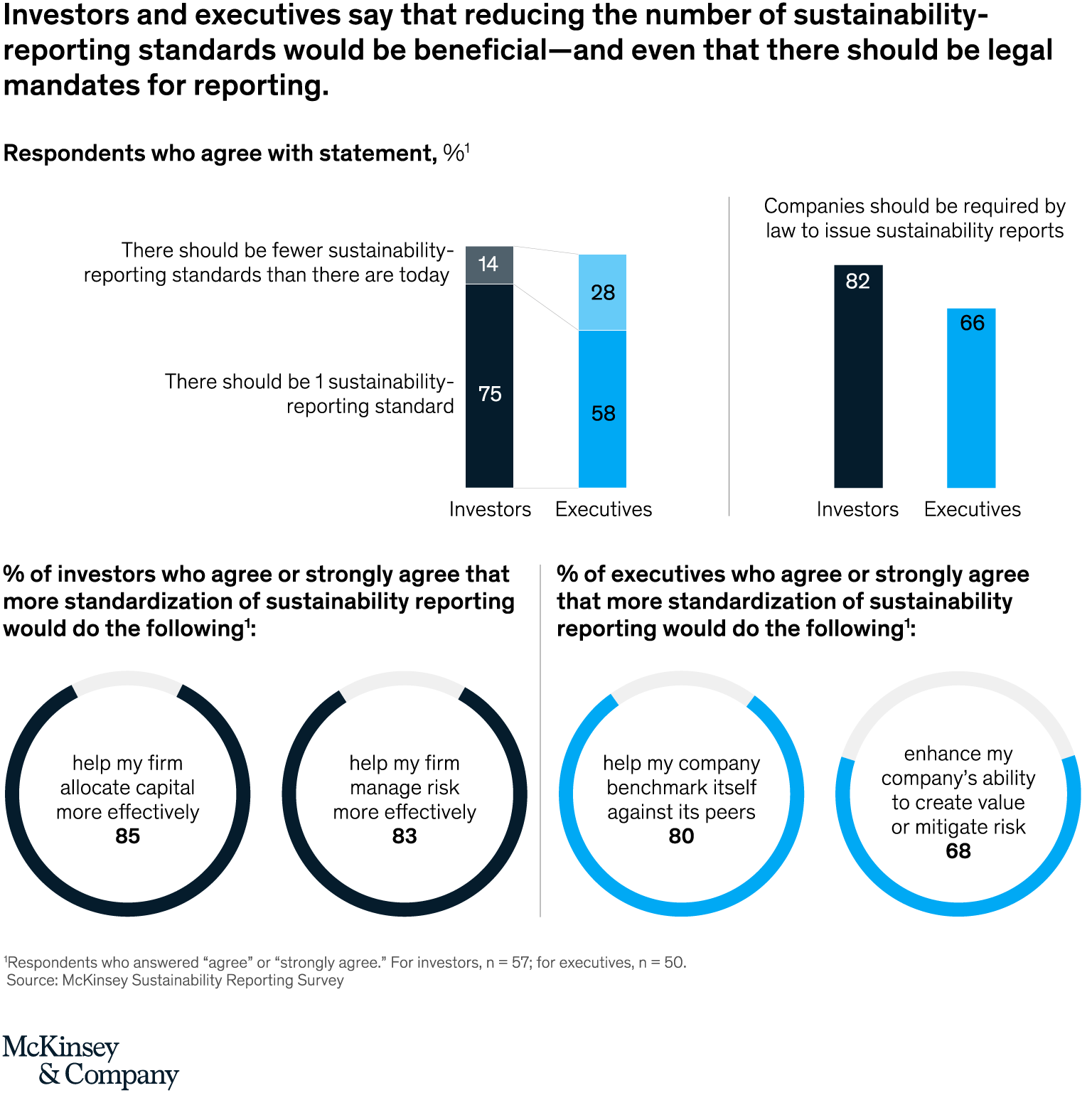

In a survey commissioned while I was at the former International Integrated Reporting Council, no fewer than 82 per cent of investors supported standardised sustainability reporting backed by regulation.

Source: McKinsey Sustainability Reporting Survey

{kind=link}

This pressure is not simply for standardisation as a process but will be exerted on both the ISSB and the European Union in finding consistency between each other in achieving it.

By 2025, one third of global investment assets and over a half of European-based assets are predicted to be in dedicated ESG funds, where understanding sustainability performance is key not simply to better risk assessment, but a clear requirement for what beneficiaries need and expect.

In addition, expect the science of measuring impact and of linkage back to financial performance to further develop at pace, which means old uncertainties about the reliability of sustainability information are fast disappearing.

Both the demand and the potential for a clear and common landscape for both the European and global initiatives, will increasingly exist.

The apparent disparity between regulatory forces behind the two initiatives may also be smaller than first appears. The IFRS Foundation was chosen as a home for international sustainability standards, precisely because its financial reporting standards are already adopted in 144 countries worldwide. Finance Ministers and Central Bank Governors from 40 countries welcomed the formation of the ISSB, ten of whom were from within Europe.

Regulators as much as investors, may be a force for convergence.

There may be a mutual interest too in ensuring both initiatives learn from each other. Just as the ISSB is committed to building on previous work of voluntary sustainability reporting frameworks and standard-setters (and has incorporated the former Value Reporting Foundation and Climate Disclosure Standards Board in its infrastructure), it should acknowledge and build on the considerable body of work undertaken in this sphere by the European Union since its first (then) Non-Financial Reporting Directive in 2014 and its decision to move towards establishing specific policies and legislation for sustainable finance in 2018.

Of the former ‘Big 5’ sustainability frameworks and standard-setters, interestingly the Global Reporting Initiative has remained independent and signed Memoranda of Understanding with both European and global standard-setters. As the leading early pioneer of sustainability reporting, it is understandable that the organisation is reluctant to merge with the initiatives, but it remains to be seen whether this can act as a ‘bridge’ between the two.

Furthermore, recent months have seen growing arguments from proponents of the ISSB that the two different approaches to materiality determination may also converge.

The International Organisation of Security Commissions’ (IOSCO) Final Report on Sustainability-related Issuer Disclosures last year, argued that it is only a matter of time when sustainability risks become financially material to the company. This has been described as ‘dynamic materiality’, in which the company’s external impacts flow into its performance and prospects.

The Chair of IOSCO has said that ‘impact’ is “highly relevant” to enterprise value creation and that he believes the differences will fade away. IFRS Trustees have also suggested that the two approaches will converge.

In the Climate Prototype which was one of the ISSB’s first initiatives, the IOSCO report finds that 28 of 34 metrics in the ‘enterprise value creation’ approach, would have also applied in multi-stakeholder metrics in accordance with the Global Reporting Initiative (GRI). The table shows our own comparison of the two, suggesting important differences remain.

A closer look reveals important differences as regards disclosures concerning the alignment of climate mitigation targets and transition plans with the goals of the Paris Agreement (1.5°C). It should be noted that both initiatives require disclosures of GHG emissions scope 1, 2, 3 and provide disclosure requirements on climate targets as such. Below, main differences are highlighted.

Analysis of the ISSB’s General Requirements Prototype, suggests that much of the content is already covered in the proposed EU standards, with small differences in terminology and architecture and arguably a slight difference in the level of ambition. The exposure drafts of each were published at the end of last month.

There are still critics who suggest that the goals of sustainable development will never be achieved using a financial materiality lens, and that without reference to the sustainability context - the ecological limits and thresholds for which sustainability is required - these processes can be rendered meaningless.

The concept of ‘dynamic materiality’ may not be sufficient, if the time taken to move sustainability impacts into the financial materiality space, comes too late.

Remember the ‘tragedy of the horizons’.

The requirement for large companies in Europe to draw up climate transition plans and the trend for companies to adopt science-based targets in alignment with the goal of limiting climate change to 1.5°C are positive signs.

There are clear indications that the standard-setters too are listening to these arguments and that perceptions may begin to change.

It has even been suggested that the ISSB’s Consultative Committee could oversee technical production of indicators on both approaches to materiality, producing a ‘superset’ which could inform both its own standards development but also that of other jurisdictions, including Europe.

The potential for this more expansive view of how the European and global standards could be more closely coordinated and complementary to each other, was backed in a public statement from 57 major companies and investors, representing over EUR 8.5 trillion in assets and employing over 5 million people, published last October. The statement backs the European process for standard-setting and believes that encouraging constructive cooperation between European and international initiatives is the best way forward.

Major players seem to be saying that they do not see a contradiction.

The real dangers of lack of convergence

Indeed, those who argue against perceived competition between EU and global standards, may be missing the point altogether.

The true lack of convergence may come on the question of U.S. based companies and investors being subject to ESG standards for company reporting. A draft on climate reporting has been produced recently by the U.S. Securities and Exchange Commission and is expected to be agreed later this year. Whilst a major step forward, it differs markedly from the proposed European and global standards. Materiality will continue to be defined with a high degree of company discretion; the draft applies to climate risk only; and there is no provision either for enforcement or for defining reporting standards.

It should be remembered that an eleven-year exercise from 2002 to try to bring the US generally accepted accounting principles into the International Financial Reporting Standards ultimately failed. This historical divergence between the United States and the rest of the world on financial reporting standards, may simply be replicated when it comes to sustainability.

Yet more than 60 per cent of global institutional investment assets and in market capitalisation of the world’s Top 100 companies are both held in the United States.

Urgent diplomatic efforts are needed at the same level of intensity as in climate change negotiations themselves, as well as pressure from domestic business and investors who are committed to the sustainability challenge, to seek to engage the United States in truly global efforts.

With uncertainty about this, it remains understandable that Europe wants to guard its own approach, to avoid the risk of its own standards being diluted.

Of similar concern must be the unanswered questions about integration between sustainability and financial reporting. A key motivation for sustainability standard-setting was to ensure reports had the same data quality as financial reports and would be trusted and used in the same level of decision-making by investors.

The IFRS Foundation remains the perfect home for this to be achieved.

However, the fact that the ISSB is being created separate from the International Accounting Standards Board and that sustainability and financial reporting will be ’connected’ rather than integrated, still risks companies’ sustainability performance being viewed as secondary in importance, disconnected to its finances and the impacts of companies continuing to be regarded as externalities.

Only when sustainability is integral to every report and every balance sheet, will sustainability objectives be genuinely pursued by the world’s business and economies.

The mantra of the previous ‘Big 5’ international sustainability frameworks and voluntary standard-setters has been for the creation of a ‘comprehensive, globally accepted, corporate reporting system’.

Without the United States and without integration, the system risks falling short in both objectives.

Those sceptical of the approach being adopted by either or both of Europe and the ISSB, should perhaps worry a little more about these challenges.

A 10-point plan for better cooperation between European and global sustainability standards

Rich and constructive debates continue to take place around all these issues, in what remains the early stages of what could be genuinely historic developments.

In the last part of this article, this author suggests ten practical ideas to contribute to the debate, which separately or collectively might assist in securing greater consistency and collaboration between the European and global standard-setting initiatives.

They can be divided into three models: initiatives which engender cooperation between the two processes, those which actually link the governance of the two and those which put them more explicitly on the path to convergence.

a) A cooperative model

1. Common intellectual property

In practice, the mutual sharing of experience, tools and content has begun to be offered, which is welcome. There may be a case to formalise this and to make explicit that the very considerable degree of intellectual property generated in the processes, will be fully shared between the two standard-setting initiatives on a continuing basis.

2. Joint consultations

Although it is reasonably certain that the two standard-setting bodies will be working on different issues at different times, there could be a genuine effort to coordinate both the timing and some of the content of their respective consultations, which are an essential part of standard-setting processes. Spacing between respective consultations would be a minimal requirement, to help generate the best responses. The ISSB could go as far as agreeing to undertake all its consultations within Europe jointly with EFRAG, to demonstrate common intent to the market and enable feedback from European stakeholders to be heard and used by both. The European Union could reference progress in the global standards, alongside all communications and discussions in its own process.

3. An Agreement.

The two organisations might quite simply negotiate a high-level agreement to commit to collaboration, to clarify and agree their respective roles. A parallel exists for product standardisation in the Vienna Agreement between the International Organisation for Standardisation and the European Committee for Standardisation, which works effectively to manage any duplication or conflict.

b) A governance model

4. Using the proposed conceptual frameworks to establish a common language

A more ambitious proposal would be to develop the respective conceptual frameworks for both initiatives in close collaboration. To the degree that consistent principles, definitions and objectives can be established within the two frameworks, this would shape alignment between the processes for many years moving ahead. It could be described as producing the ‘common language’ which companies and investors would prefer. A single conceptual framework between the two would be even more ground-breaking, but does not appear possible. The European Union has already produced an early draft in the form of a working paper. However, a common approach to application and interpretation of each set of standards, founded by aligning their respective conceptual frameworks as far as possible, can be realistic.

5. A joint technical coordination mechanism.

In practice, most inconsistencies would not be intentional, but the product of the different processes and able to be resolved at the level of technical specialists, to which either side could refer. The ISSB may be cautious about treating Europe differently from its consultations with other jurisdictions in the world. However, given Europe’s advanced timetable and the maturity of its proposals, such a joint mechanism could be a pragmatic solution, which could always be offered to other regions in later years.

6. A settlement mechanism.

A variant of this approach, which was proposed by the Association of Chartered Certified Accountants, would be to establish an independent mechanism for assessing equivalence between the different sets of standards and to be able to resolve disputes between them. Given the governance processes in which they exist, it is difficult to foresee either the European Union or the ISSB agreeing to cede such power. ACCA suggests it would need the weight of an established multilateral organisation such as the OECD, to achieve it.

7. A double-hatted Board role

A more ambitious proposal again would be to appoint a single Board member for both organisations, who would be given a specific remit to promote coordination between the two. Differences in the governance structure on the European side, may make that more complicated. But the backgrounds and motivations of Board members in both initiatives, will play a decisive role in how far to engage in this and the other coordination ideas suggested.

c) A convergence model

8. An explicit commitment to convergence

There has been much talk of convergence from both standard-setters and the European Commission has already pledged to work towards this objective. How far and how quickly it can be achieved, remains another open question. However, the very commitment would provide confidence in the market and is likely to have an important influence on all actors within the processes. A key question to the ISSB will be in how far it will move in future to incorporate ‘impact’ into its materiality definition.

9. Adopting the principle of interoperability

This was much discussed in our efforts to align voluntary sustainability frameworks and standard-setters and can be criticised as “having to do both” rather than achieving genuine alignment. The concept of interoperability simply means that standard-setters work for the two sets of standards to be as complementary as possible. Anything which can assist report preparers to avoid unnecessary duplication and to enable single data sets to inform company reporting according to different standards, has a genuine benefit for companies.

10. A commitment to reciprocity

Perhaps the most sensitive question goes back to who is driving the car? Some have suggested that the ISSB should have the prerogative in developing standards using the ‘enterprise value creation’ lens and that Europe should confine itself to standards based on impact to stakeholders exclusively. The Institute for Chartered Accountants in England and Wales suggested that Europe and other jurisdictions could ‘apply’ to the ISSB to develop a particular standard (including impact standards), and only do so on its own initiative, if the ISSB chose not to do so.

Given the standards, policies and governance which are arguably unique in the European Union amongst inter-governmental organisations in the world, these ideas are unlikely to be taken up in Brussels and can be questioned in terms of workability in any case. The EU’s own global reach should not be under-estimated, not simply to enforce corporate reporting standards on foreign entities through its trade powers, but in its own global diplomacy with other jurisdictions. This is evidenced by the work of the International Platform on Sustainable Finance established by the European Commission in 2019, and which has already heralded the beginning of efforts to forge common sustainability standards with China.

The ISSB will naturally want to uphold the leadership role on global standards, and the European Union has been quite ready to respect the primacy of the international approach in relation to product standardisation. However, the idea of primacy is likely to inhibit rather than foster collaboration and it may be better for the two standard-setting initiatives instead, to commit to what might be called the principle of ‘reciprocity’. This would go further than the idea of exchange between the two, to represent a concept which would focus on mutual respect, the desire for complementarity at all levels and a commitment to mutually self-supporting actions. The European Union would go as far as suggesting that this is called ‘co-construction’. The ‘reciprocity’ label may be more acceptable to the ISSB, as it would not be suggested there would be equality between the two, but that each would be working hand-in-hand.

To extend the analogy: both would have their hands on the wheel.

Conclusion

This last idea, as with the others, is highly dependent on the culture which will be created between the two organisations and the key individuals involved. They are offered in a spirit of openness and joint endeavour which will be required. Success is also dependent on the ability of all involved to seize the enormity of the sustainability challenge and to see that the necessity of collective action between many different actors across the spectrum, far outweighs traditional thinking based on institutional rivalries.

From the point of view of companies and investors, let alone wider stakeholders, it remains important to recognise the unprecedentedly fast progress which is being made on sustainability standards, compared to all past similar processes. Perhaps the most important signal to the two standard-setters is to maintain and intensify this momentum in what they are doing.

Similarly, it should be recalled that EFRAG started by looking at 200 different sustainability standards for business at the sectoral, national as well as international level. The International Trade Centre catalogues some 2,500 standards and related initiatives in the field of corporate sustainability and of Responsible Business Conduct.

If the world manages to simplify this to two or only a handful of major initiatives rather than one, it could be said that the aspiration to clarify the landscape will indeed still have been achieved.

Finally, never forget that the benefit of standards processes comes only in that they are used. It is the ‘acceptance’ of a standard, which is necessary for its existence.

So companies, investors, stakeholders and regulators will assess the new standards for themselves and perhaps will be the ultimate deciders on how and if European and global sustainability standards work together.

I hope they will.